In the market for a new car? Maybe you’ve grown tired of the one you already own and have decided that it’s time for an upgrade. Last week I received this question from one of my followers and thought it was a solid topic to dissect. Once and for all I’m going to lay this whole “should I buy, used, new or lease argument” to rest. At least, from my point of view.

I actually haven’t made a car payment in over two years and it’s been awesome, so I’ve been pretty far removed from “shiny, new toy syndrome” for a while now. Since I haven’t been in the market for a new car in quiet some time, I had no idea how much cars are costing folks these days, so I did a little digging. Originally, I figured that the average cost of a new car these days had to be right around $27,000, but apparently, I was way off.

According to an article published by USA today, an analysis of auto loans conducted by Experian found that the average new vehicle loan hit a record high of $31,099; the average loan for a used car (or automobile) climbed to a record of $19,589 in 2017. But all of these facts and figures can seem pretty mind-numbingly boring if you’re unable to conceptualize how they apply to you. I mean who really knows at the end of the day if you’re throwing money out the window by leasing a car or if in fact, a used car is your best option.

In order to help you figure out how all these numbers apply to you and any future car purchases you may have, below I created an as “true to life” example I could think of, to help you also resolve the whole debate for yourself.

Before we dive into the below example, I want to make it clear that this post and example revolves around the average person. The average person meaning someone that walks into a dealership with the intent to finance a car or already has an approved car loan through his/her bank to purchase a car. I think its safe to say, however, that everyone would agree that the best way to buy a car is to save, buy used, and pay cash. I do understand, however, that paying cash for a reliable vehicle isn’t everyone’s cards.

Let’s say you’ve been eying a 2018 Toyota Corolla that you plan on buying new and owning for 8 years. You are also willing to consider buying the 2017 model of the new car you’re eying, as long as it comes with a majority of the same features and doesn’t have a lot of miles on it. After some extensive research (wink wink) you learn that the Corolla has expectational safety reviews, great gas mileage, and oh yeah, can well exceed 150,000 miles with proper care and maintenance, basically, this is a car you can drive until the wheels fall off.

You’ve been unsure about whether or not you should buy used, new, or lease the car, like any good member of the Make Real Cents tribe, you run the numbers on all three scenarios to figure out what will work best for you and your budget.

Lease:

The dealer down the street is running a leasing deal on all 2018 Toyota Corolla LE models.

- Payment Info: $159 per month for 36 months with $2,499 due at signing

- Cost Over the course of the lease: ($159 x 36 months = $5,724) + $2,499 Due at signing. Provided that you stay under the 12,000 mile yearly limit, it will cost you $8,223 over the course of 3 years or 36 months to lease a new 2018 Toyota Corolla.

- Total Cost of the Lease over 3 years: $8,223 over 3 years

- Total over 8 years: $8,223 + $8,223 + $5482 (a total of 7.5 years) = $21,928

So far you can lease a car for 3 years for a total cost of $8,223 but you will need another two leases to make up for 8 years total. Once the 8 years is up, you will then need another car and will have already spent $21,928 on the latest and greatest cars and will have a car payment for AT LEAST 8 YEARS!

Buy New:

You go on Kelley Blue Book and see that they list a brand new 2018 Toyota Corolla LE in your area for $17,784. You are looking to compare each scenario as closely as possible so you walk into the dealership with all the necessary credit documents to get some financing/a loan for your new car.

- Payment Info: Loan Amount: $17,784, Interest Rate = 3.71%, Term of Loan= 36 Month, the dealer says that your payment will come to $523 a month. He may even try to entice you into a longer loan period to get your payments down, so let’s say he throws out 60 months which would bring your payment to $325 and you think to yourself…well, I CAN AFFORD THAT.

- Tax, tag, title, registration, dealer fees, etc.: For example purposes let’s say all these fees equals a flat $1,000. These fees are largely dependent upon what state you live in but for now, let’s run with $1,000 bucks, you saved for this very moment.

- Total cost of a 36 month loan @ 3.17%= $18,819

- Total cost of a 60 month loan @ 3.17%= $19,512

- Total Cost to own the car in 3 years: Approximately $19,819 (36 months loan + tax, tag, title, excludes maintaince fees, etc.) or $20,512 over (60 months+ tax, tag, title, excludes maintaince fees, etc.)

So far you can lease a brand new car for three years for a total of $8,223, but at the end of those three years, you’ll need another car. Your other option is to buy a brand new car and have it paid off in three years, even though the payments will be a little higher for a total of $18,819. Essentially, it will cost you $10,596 more to own a car and not have to make another payment for 5 years.

Buy Used:

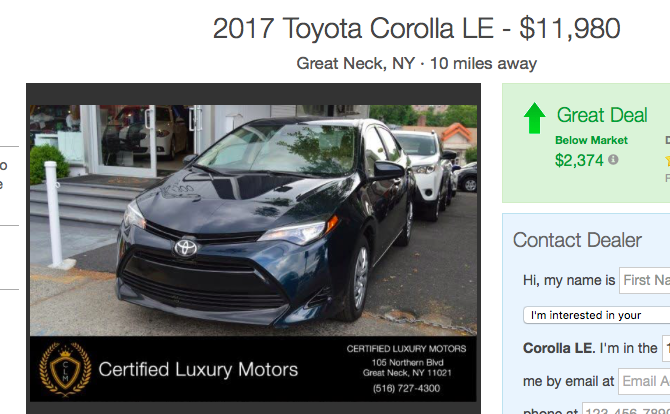

You’ve been shopping around and can’t find a hardly used 2018 because well, we’re in 2018. So you start to explore 2017 cars and come across an excellent 2018 LE equivalent, a used 2017 Toyota Corolla LE – $11,980 10 miles away from you! It has 24,000 miles on it, so it’s almost like new, one owner, no accidents, and has almost all the exact same features as the 2018 model you’ve been eyeing except a leather steering wheel cover. By the way, if you are currently in the market for a used car, Cargurus.com is an excellent tool for finding used cars in your area. Their search engine list all the cars within a specificed radius, similiar models and whether or not you’re getting a great, good, fair, or bad deal for the car.

- Payment Info: Loan Amount: $11,980, Interest Rate = 3.71%, Term of Loan= 36 months, the dealer says that your payment will come to $219 a month.

- Tax, tag, title, registration, dealer fees, etc.: For example purposes let’s say all these fees equals a flat $600. These fees are largely dependent upon what state you live in but for now let’s run with $600 bucks, you saved for this very moment.

- Total cost of a 36 month loan @ 3.17%= $13,144

- Total Cost to own the car in 3 years: Approximately $14,144 (36 months loan + tax, tag, title,excludes maintaince fees, etc.)

You compile a quick recap of all the scenarios, again reminding yourself that this is a big decision and that whatever choice you make, you intended on sticking with it for 8 years.

Eight years isn’t a crazy long time if you consider the fact that the average age of vehicles is 11.5 years. This equates to nearly one out of every four vehicles in the U.S. having been built before the year 2000, according to an article published by CNBC in 2015. Consumer reports shows that a Toyota Corolla has been proven, with regular maintenance, to get over 200k miles.

The average number of miles driven per year, according to the U.S. Department of Transportation Federal Highway Administration (FHWA) is 13,476 miles. If you plan on owning the car for 8 years, you can easily get over 20,000 miles on this car and have room to spare (20k *8 years = 160,000 miles).

But that’s just one side of the story, you also want to check out what the estimated appreciation on each car will be for fun and giggles:

VS.

To sum up what my research is actually telling me:

1.) At the end of a lease I won’t have anything to show for it, just the experience of essentially test driving a car for 3 years.

2.) With all things being equal, it will cost me $5,675 dollars more to buy a new car just to only have it be worth $985 dollars more than if I purcahsed a used car at the end of owning it for 8 years.

3.) Leasing a car over 8 years, provided that I stay within the allotted number of yearly miles, will cost me more than buying a used or new car, and I still won’t have some sort of semi-liquid asset to sell if I get in a bind. I might as well throw $21,000 dollars out the window.

4.) If I can pay my car off, new or used, I will have 5 years of cash that would have been otherwise going towards a car payment that can now to go towards my retirement. If I buy new that means $6,276 dollars extra or if I buy used $2,628 extra a year that can go towards my retirement.

5.) At the end of year 8 for both the used and new scenarios, if I, in fact, own the car, I still have something that holds value, even if it is a depreciating asset.

6.) It’s important to make the right decision when it comes to something that isn’t really going to add to your bottom line or your future. Not to mention, there are a ton of other costs associated with owning a car (Registration Cost, Car Insurance, Gas, maintenance) that will eat away money you can be putting towards retirement, so the lower you can keep your cost, the biggest being the price tag of the car, the better.

The intention of this article is to help you conceptualize a purchase, some of us, tend to approach pretty lightly. We get bored with our 4-year-old car, get “shiny new toy envy”, and BAM!, find ourselves in the dealership starting the cycle all over again. This article was designed to provide you with solid, real numbers and proof to support the belief you’ve come to know as the truth, whether that be it’s best to buy used, new or lease. This structure is a better system than just hanging your hat on “well my dad said leasing a car is much better than owning in the long run.”

Ultimately, it’s up to you to decide what works best for you and your situation but before you sign, make sure you do your homework!

Questions for you

1.) Have you ever paid off a car in full?

2.) Which option do you think is best?

3.) Do you consider a car to be an asset?

Other post you might enjoy

Subscribe

To receive 14 Free Budget Sheets and emails on the latest and greatest from Make Real Cents!

{kind=link}

Thank you so much for this information ! Very helpful for the future decisions I will be making.

Last year, I bought a 2015 Toyota Camry hybrid that was a one-owner, 2 year old used car. I paid approximately 60% of the new car price, it had 41,500 miles, and I was able to pay off my loan in under 3 months.

So to answer your 3 questions: yes I have paid off my car, used is SO SCREAMINGLY OBVIOUS the best choice, and I do believe a car is an asset. To expand on #3, I can sell it if I really needed the cash, but I can also put it to work for me in my Uber side hustle, thereby generating additional income during my commute and other leisure time.